What is Debt Collection? A Simple Guide for Business Owners

If you run a business, chances are you've dealt with a customer who didn’t pay on time—or at all. It’s frustrating, time-consuming, and it directly impacts your cash flow. That’s where debt collection comes in. But what exactly is debt collection, and how does it work?

Could Your Type of Business Benefit From Online Debt Collection?

It’s an annoying fact of life but some businesses and industries are prone to needing debt collection support more than others. Is your business one of these? Let’s take a look at whether your type of business is more likely to need a helping hand from online debt collection services like iCollect.

Customer Service and Debt Collection Aren’t Mutually Exclusive

Late payment by a customer and needing to implement debt collection techniques doesn’t by any means need to be the end of your business relationship. In fact, done in the right way, it can help preserve your dealings with them for the long-term.

The Fine Art of Writing a Debt Collection Letter

If your business is struggling with late paying clients or overdue unpaid invoices, your first official port of call in the debt collection process is to issue a debt collection letter – or a letter of demand. This comes into play when the debtor is overdue with payment.

The Certainty of Debt Collection Success vs Knowing the End Score of a Game

In the world of sports, every team strives for victory, driven by strategy, skill, and teamwork. Similarly, businesses aim to achieve success, especially in debt collection and debt recovery efforts. While the outcomes may differ—one being a predetermined score and the other an ongoing effort—the principles for success in both very similar.

How Payment Plans Elevate Your Debt Management Strategies

Are you struggling to get debtors to pay the full amount of their invoice? If so, the secret to success could be to offer an accessible payment avenue for debtors with structured payment plans. As they say a bird in the hand is worth more than two in the bush, so even part payment this month is better for your books than no payment at all!

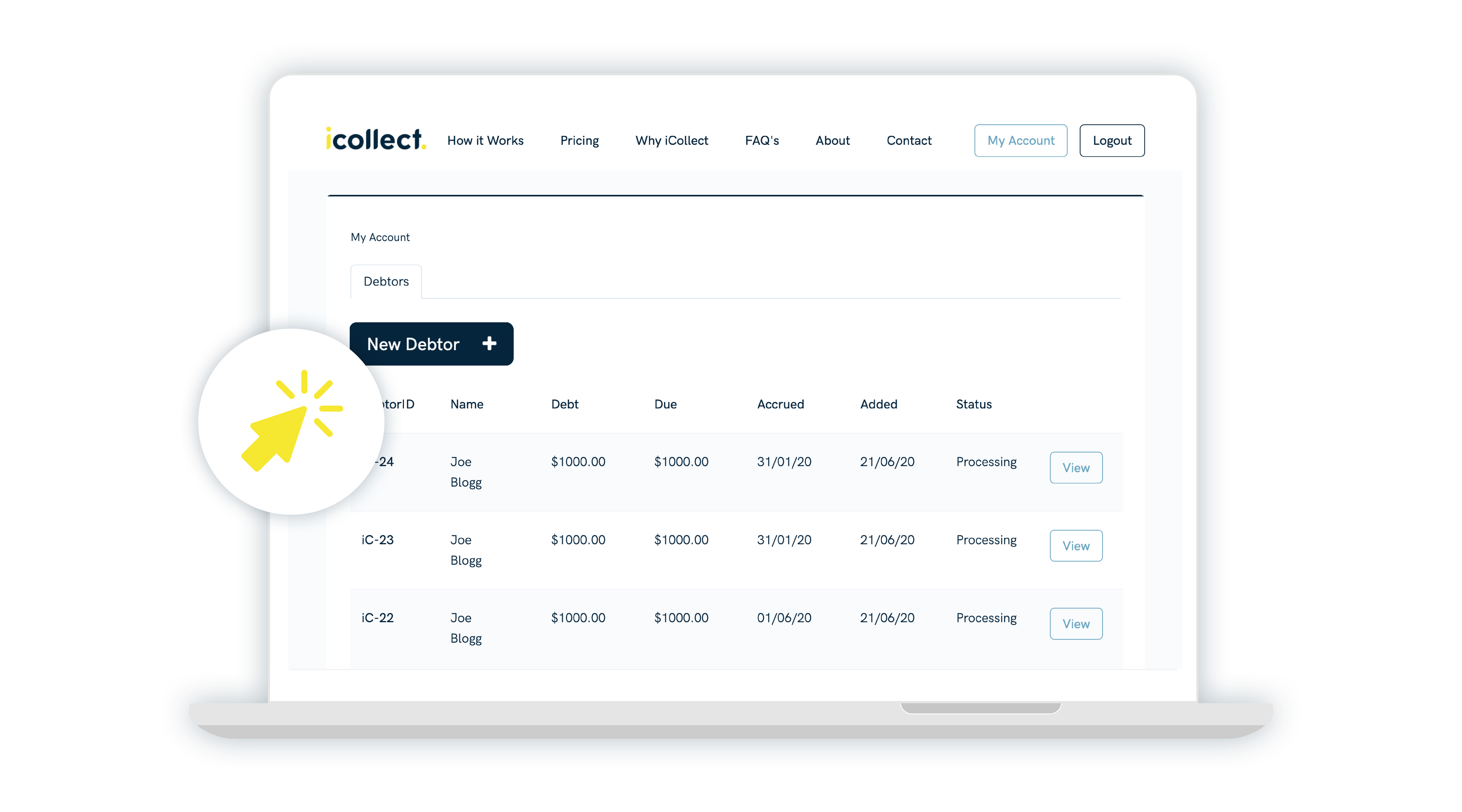

Why You Should Automate Your Business's Debt Recovery

As a business owner, you’ll know that one of the scarcest resources is time. This is particularly true if you are spending valuable hours recovering debts. But now, there’s a better way to ensure your invoices are being paid while giving you time back to spend on your business – automating your debt recovery process.

Keep your customers returning, even after debt collection

Late payment by a customer and needing to implement debt collection techniques doesn’t by any means need to be the end of your business relationship. In fact, done in the right way, it can help preserve your dealings with them for the long-term.